Value Assessment Framework

The ICER value framework describes the conceptual framework and set of associated methods that guide the development of ICER evidence reports. The purpose of the value framework is to form the backbone of rigorous, transparent evidence reports that, as a basis for broader stakeholder and public engagement, will help the United States evolve toward a health care system that provides sustainable access to high-value care for all patients.

In 2023, the process of updating ICER’s value assessment framework included extensive benchmarking with health technology assessment (HTA) organizations around the world and consideration of input from numerous organizations and individuals across the US health system. During this process, ICER received feedback from over 30 organizations.

- The 2023 Value Assessment Framework

- The 2023 Processes for Conducting Value Assessment

- The 2023 Value Assessment Framework Webinar and Webinar Slides

- ICER Reference Case for Economic Evaluations

- ICER-PHTI Assessment Framework for Digital Health Technologies

- Considering Clinical, Real-World, and Unpublished Evidence

- For treatments for ultra-rare, serious disease, please see ICER’s framework adaptations

- For therapies that may be potential cures, please see ICER’s white paper on potential cures

- For therapies that may treat COVID-19, please see ICER’s adaptations for evaluating price during a pandemic

- Nominate a topic for ICER to review

- Perspective on Cost-Effectiveness Threshold Ranges

- Adaptations to ICER’s Process (October 2020)

President Steven Pearson, MD, MSc, and President-Elect Sarah Emond, MPP, summarized the philosophy behind ICER’s approach to value assessment, as well as several key updates that will be implemented in the near term. Watch a recording of the webinar. Please find the accompanying slide deck here.

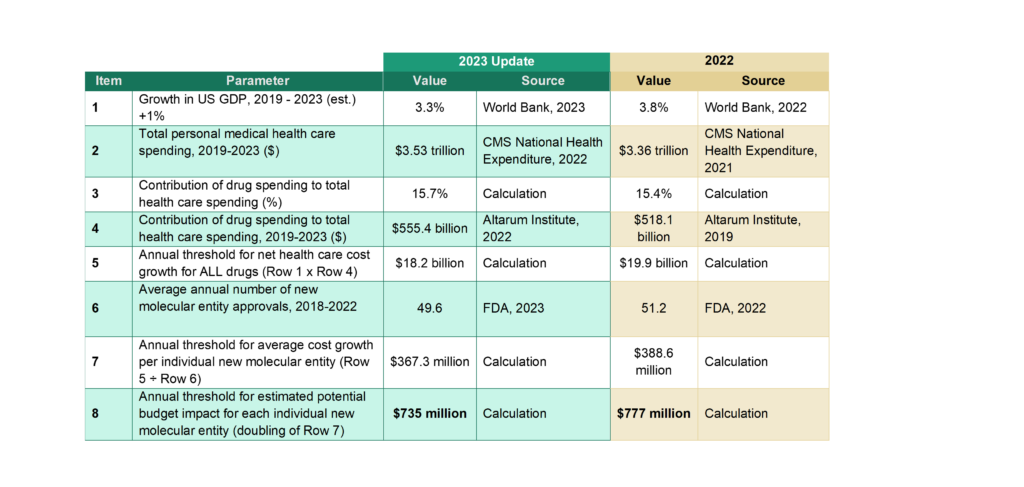

Potential Budget Impact Threshold Updated for 2023-2024

ICER is committed to ensuring its methods and processes are aligned with current information on the health care environment in the US. In August 2023, ICER updated its annual budget impact threshold for prescription drug therapies from $777 million to $735 million. This update reflects the running five-year average annual number of FDA new drug approvals, as well as estimates for current overall US medical spending, spending on prescription drugs and drugs administered by providers, and the five-year average annual growth in gross domestic product (GDP). We note that the change in GDP was negative when comparing 2020 to 2019, but instead of using a negative GDP percent change value, we again assigned a 0% change for the year 2020 to moderate the impact that the COVID pandemic has on our updated estimates.

When clinical experts involved in the ICER review suggest that uptake of a new drug over a five-year period should be at a level that would likely exceed our potential budget impact threshold, ICER’s report will highlight the risk for short-term affordability and associated access challenges that should be addressed by policymakers. The report will also include the maximum percentage of eligible patients who would be able to receive the therapy, at multiple possible price points, without exceeding the threshold. However, the intent of the budget impact analysis is neither to provide a precise projection of likely market nor to provide estimates of commonly reported budget impact metrics (e.g., net cost per-member per-month).

The budget impact threshold will continue to be calculated as double the average net budget impact that would contribute to overall health care cost growth exceeding current growth in the US economy. Updated calculations with sources for data are shown below.

* Growth in US GDP was set to 0% for the 2020 year (real change in GDP was negative due to the global pandemic)

Adaptation of the ICER value framework for the assessment of treatments for ultra-rare conditions

ICER’s modified framework for ultra-rare conditions is the culmination of a nine-month public process of engagement with the rare disease patient community, the life sciences industry, and US health care payers. We updated the framework in 2020. As part of this process, ICER published a white paper discussing the evidentiary and ethical challenges associated with evaluating treatments for rare conditions, hosted a multi-stakeholder policy summit, and accepted public comment from more than 50 organizations and individuals regarding an initial proposal of framework modifications. ICER looks forward to ongoing input from the entire stakeholder community and launched a formal update to these methods in 2019.

Addendum for Assessment of Potential Cures

ICER is aware that questions are being raised about the best way to assess the cost-effectiveness and calculate value-based prices for emerging treatments that are considered to be potential cures. Some would argue that potential cures offer benefits incompletely captured by traditional utility measurements related to the added well-being patients and families realize from being “free” from disease. Many have noted that cost-effectiveness analyses of potential cures are particularly sensitive to assumptions about the durability of clinical benefit beyond the available short-term data. And others have raised concerns that, without some modification, traditional cost-effectiveness methods would assign an unrealistically high price to a potential cure for conditions such as hemophilia or some cancers currently associated with very high lifetime treatment costs.

Given these issues, ICER will continue to seek input from all stakeholders on the key assumptions that will be used to guide the base case cost-effectiveness analysis in any review. If a potential cure is selected for review, ICER may also consider various novel approaches to address the issues described above. In order to produce reports that can be most useful to inform policy making, ICER may therefore test and implement new methods for calculating value-based prices for potential cures.

ICER 2019 Perspectives on Cost-Effectiveness Threshold Ranges

ICER conducted a seminar series in 2019 to share perspectives and inform thinking among academics and Health Technology Assessment (HTA) programs on approaches to determining operative cost-effectiveness thresholds for decision-making in health care. Health economists from around the world participated, with presentations from leading figures including Karl Claxton, PhD, MSc, from the University of York; Jens Grueger, PhD, from F. Hoffmann-La Roche & University of Washington; Sean Sullivan, PhD, MS, from the University of Washington; and Chris McCabe, PhD, MSc, from the University of Alberta. Read the perspectives on cost-effectiveness threshold ranges here.